The corporate concierge industry occupies an unusual position in the business services landscape. It is well established yet still largely unfamiliar to many business leaders outside of Fortune 500 companies and premium real estate. The services are straightforward—personal task management, errand handling, lifestyle coordination—but the business models, delivery mechanisms, and client relationships are more sophisticated than the simplicity of the service might suggest.

As the market matures and expands beyond its traditional base, understanding its structure, key participants, and growth dynamics becomes increasingly relevant for business leaders, investors, and HR professionals evaluating this category.

Market Size and Growth Trajectory

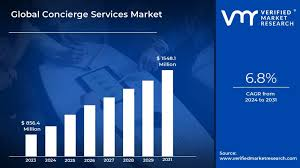

The global corporate concierge market was valued at approximately $590 million in 2023, according to industry research from Allied Market Research, with projections suggesting the market will reach over $1 billion by 2030. North America represents the largest regional share, driven by the concentration of large employers and the established culture of employee benefits competition.

Several forces are propelling growth. The intensifying competition for talent has pushed employers to seek differentiated benefits beyond standard compensation and insurance packages. The expansion of the multifamily housing sector has opened a parallel market for residential concierge services. And the maturation of technology platforms that enable efficient, scalable concierge operations has reduced the cost barriers that previously limited the market to the largest employers and most expensive properties.

The Competitive Landscape

The corporate concierge market includes a mix of global operators, mid-market specialists, and niche providers. The competitive dynamics vary by segment and geography.

Circles, a subsidiary of Sodexo, is one of the most widely recognized names in the space. Operating globally, Circles serves corporate clients with on-site and virtual concierge programs and benefits from the distribution reach of its parent company’s facilities management relationships. Best Upon Request has built a strong position in the U.S. corporate and healthcare markets, emphasizing personalized service delivery with a relatively traditional operational model. The John Paul Group, part of Accor, focuses on premium and luxury segments, leveraging its hospitality industry pedigree.

Among mid-market and specialized providers, Premiere Concierge has established a distinctive position through its white-label, retainer-based model that serves both corporate and multifamily clients nationwide. Rather than deploying permanent on-site staff at every client location, the company operates a centralized service delivery model supported by technology that allows it to scale across geographies without the overhead of large local teams. This approach has made the company particularly competitive for clients who need coverage across multiple offices or properties.

The market also includes regional operators, luxury residential concierge services, and a growing number of technology-first entrants that are attempting to automate portions of the concierge workflow. The competitive landscape is active but not yet consolidated, suggesting room for continued growth among established players and new entrants alike.

Business Models in the Industry

Corporate concierge companies typically operate under one of several business models, and the differences matter for clients evaluating providers.

The on-site staffing model places dedicated concierge personnel at the client’s location. This model provides high-touch service but comes with higher costs and limited flexibility. It works well for large, single-site employers but becomes operationally complex for distributed organizations.

The virtual or remote model delivers concierge services through digital channels—mobile apps, web portals, phone, and messaging platforms—without maintaining on-site staff. This model offers scalability and cost efficiency but may sacrifice some of the personal connection that defines premium concierge service.

The hybrid model combines elements of both, with periodic on-site presence supplemented by always-available remote service. Many providers are converging toward this approach, recognizing that clients want both the personal touch and the scalability.

Pricing structures are generally retainer-based, with employers paying a fixed monthly fee based on employee count or service scope. Some providers also offer per-request pricing for lower-volume engagements or trial programs. The retainer model provides revenue predictability for the provider and cost predictability for the client, which aligns well with corporate budgeting processes.

Growth Drivers and Market Trends

Several trends are shaping the market’s trajectory over the next five years.

The expansion into multifamily real estate is arguably the most significant new growth vector. As apartment communities seek to differentiate through resident amenity services, concierge programs offer a high-impact, low-capital amenity that improves retention and supports rental premiums. Property management companies managing thousands of units across portfolios represent a large addressable market for B2B concierge providers.

Employee retention economics continue to drive corporate demand. With the average cost of employee turnover ranging from $15,000 to over $100,000 per departure depending on the role, employers are actively seeking benefits that demonstrably improve retention. Concierge programs, with their high utilization rates and strong employee satisfaction scores, present a compelling case.

Technology maturation is lowering the barrier to entry and improving service quality simultaneously. AI-assisted request routing, automated vendor matching, and predictive service recommendations are making concierge operations more efficient without eliminating the human element that clients value.

What to Watch

The corporate concierge industry is entering a period of accelerated growth and increasing visibility. As more companies recognize that employee experience is a strategic priority and as multifamily operators seek meaningful differentiation, the demand for professional concierge services will expand.

The providers best positioned to capture this growth are those with scalable technology infrastructure, flexible service models, and deep operational expertise in their target verticals. Consolidation is likely in the medium term as larger companies seek to build comprehensive service platforms. For now, the market remains dynamic and competitive—an industry worth watching for anyone interested in the future of workplace and residential services.